Banking and Indian Financial System

Important Concepts:

Benefits of Mutual Funds

Functions of NABARD

Short Note on Venture Capital

Functions of Stock Exchange

Importance of Commercial Bill Market

Non-Banking Finance Companies

Functions of Merchant Bankers

Financial Services in Commercial Banks

Role of Commercial Bank in the development of industry

Role of Merchant Bankers

Importance of Indian Capital Market

Role of NABARD

Growth and Development of SEBI

Difference b/w Hire purchase and Leasing

Role of Foreign Investment in India

Part A Q&A:

1. What is the importance of banking services in the

development of an economy?

1.

Capital Formation

Banks

play an important role in capital formation, which is essential for the

economic development of a country. They mobilize the small savings of the

people scattered over a wide area through their network of branches all over

the country and make it available for productive purposes.

Now-a-days,

banks offer very attractive schemes to attract the people to save their money

with them and bring the savings mobilized to the organized money market. If the banks do not perform this function,

savings either remains idle or used in creating assets, which are low in scale

of plan priorities.

2.

Creation of Credit

Banks

create credit for the purpose of providing more funds for development projects.

Credit creation leads to increased production, employment, sales and prices and

thereby they cause faster economic development.

3.

Channelizing the Funds to Productive Investment

Banks

invest the savings mobilized by them for productive purposes. Capital formation

is not the only function of commercial banks. Pooled savings should be

distributed to various sectors of the economy with a view to increase the

productivity of the nation. Then only it can be said to have performed an

important role in the economic development of the nation.

Commercial

Banks aid the economic development of the nation through the capital formed by

them. In India, loan lending operation of commercial banks subject to the

control of the RBI. So our banks cannot lend loan, as they like.

4.

Fuller Utilization of Resources

Savings

pooled by banks are utilized to a greater extent for development purposes of

various regions in the country. It ensures fuller utilization of resources.

5. Encouraging Right Type of

Industries

The banks help in the

development of the right type of industries by extending loan to right type of

persons. In this way, they help not only for industrialization of the country

but also for the economic development of the country. They grant loans and

advances to manufacturers whose products are in great demand. The manufacturers

in turn increase their products by introducing new methods of production and

assist in raising the national income of the country.

6. Bank Rate Policy

Economists are of the

view that by changing the bank rates, changes can be made in the money supply

of a country. In our country, the RBI regulates the rate of interest to be paid

by banks for the deposits accepted by them and also the rate of interest to be

charged by them on the loans granted by them.

7. Bank Monetize Debt

Commercial banks

transform the loan to be repaid after a certain period into cash, which can be

immediately used for business activities. Manufacturers and wholesale traders

cannot increase their sales without selling goods on credit basis. But credit

sales may lead to locking up of capital. As a result, production may also be

reduced. As banks are lending money by discounting bills of exchange,

business concerns are able to carry out the economic activities without any

interruption.

8. Finance to Government

Government is acting as

the promoter of industries in underdeveloped countries for which finance is

needed for it. Banks provide long-term credit to

Government by investing their funds in Government securities and short-term

finance by purchasing Treasury Bills.

9. Bankers as Employers

After the

nationalization of big banks, banking industry has grown to a great extent.

Bank’s branches are opened in almost all the villages, which leads to the

creation of new employment opportunities. Banks are also improving people for

occupying various posts in their office.

10. Banks are Entrepreneurs

In recent days, banks

have assumed the role of developing entrepreneurship particularly in developing

countries like India. Developing of entrepreneurship is a complex process. It includes

the formation of project ideas, identification of specific projects suitable to

local conditions, inducing new entrepreneurs to take up these well-formulated

projects and provision of counselling services like technical and managerial

guidance.

Banks provide 100% credit for worthwhile projects,

which is also technically feasible and economically viable. Thus commercial

banks help for the development of entrepreneurship in the country.

2. What is the role of RBI in Cooperative credit to

weaker section?

i.

Target

for lending to total priority sector and weaker section will continue as 40 per

cent and 10 per cent, respectively, of Adjusted Net Bank Credit (ANBC) or

credit equivalent of off-balance sheet exposure, whichever is higher, as

hitherto.

ii.

Agriculture:

Distinction between direct and indirect agriculture is dispensed with.

iii.

Bank

loans to food and agro processing units will form part of Agriculture.

iv.

Medium

Enterprises, Social Infrastructure and Renewable Energy will form part of

priority sector.

v.

A target

of 7.5 per cent of ANBC or credit equivalent of off-balance sheet exposure,

whichever is higher, has been

prescribed for Micro Enterprises.

vi.

Education:

Distinction between loans for education in India and abroad is dispensed with.

vii.

Micro

Credit ceases to be a separate

category under priority sector.

viii.

Loan

limits for housing loans qualifying under priority sector have been revised.

ix.

Priority

Sector assessment will be monitored through quarterly and annual statements.

3. What do you mean by non- Banking Finance

Company?(Guide pgno 24)

A

Non-Banking Financial Company (NBFC) is a company registered under the

Companies Act, 1956 engaged in the business of loans and advances, acquisition

of shares/stocks/bonds/debentures/securities issued by Government or local

authority or other marketable securities of a like nature, leasing,

hire-purchase, insurance business, chit business but does not include any

institution whose principal business is that of agriculture activity,

industrial activity, purchase or sale of any goods (other than securities) or

providing any services and sale/purchase/construction of immovable property. A

non-banking institution which is a company and has principal business of

receiving deposits under any scheme or arrangement in one lump sum or in

instalments by way of contributions or in any other manner, is also a

non-banking financial company (Residuary non-banking company).

4. Describe the different kinds of mutual funds?

> Open-ended funds

In an open-ended mutual

fund, an investor can invest or enter and redeem or exit at any point of time.

It does not have a fixed maturity period.

> Close-ended funds

Close-ended mutual

funds have a fixed maturity date. An investor can only invest or enter in these

type of schemes during the initial period known as the New Fund Offer or NFO

period. His/her investment will automatically be redeemed on the maturity date.

They are listed on stock exchange(s).

Let's take a look at the

various types of equity and debt mutual funds available in India:

1. Equity or growth schemes

These are one of the most popular mutual fund schemes.

They allow investors to participate in stock markets. Though categorised as

high risk, these schemes also have a high return potential in the long run.

They are ideal for investors in their prime earning stage, looking to build a

portfolio that gives them superior returns over the long-term. Normally an

equity fund or diversified equity fund as it is commonly called invests over a

range of sectors to distribute the risk.

Equity funds can be further

divided into three categories:

> Sector-specific

funds:

These are mutual funds that invest in a specific

sector. These can be sectors like infrastructure, banking, mining, etc. or

specific segments like mid-cap, small-cap or large-cap segments. They are

suitable for investors having a high risk appetite and have the potential to

give high returns.

> Index funds:

Index funds are ideal for investors who want to invest

in equity mutual funds but at the same time don't want to depend on the fund manager.

An index mutual fund follows the same strategy as the index it is based on.

For example, if an index fund

follows the BSE Index as the replicating index and if it has a 20% weightage in

let's say Stock A, then the index fund will also invest 20% of its assets in

Stock A.

Index funds promise returns in line with the index

they mirror. Further, they also limit the loss to the proportional loss of the

index they follows, making them suitable for investors with a medium risk

appetite.

> Tax saving funds:

These funds offer tax

benefits to investors. They invest in equities and are also called Equity

Linked Saving Schemes (ELSS). These type of schemes have a 3 year lock-in

period. The investments in the scheme are eligible for tax deduction u/s 80C of

the Income-Tax Act, 1961.

2. Money market funds or liquid funds:

These funds invest in short-term debt instruments,

looking to give a reasonable return to investors over a short period of time.

These funds are suitable for investors with a low risk appetite who are looking

at parking their surplus funds over a short-term. These are an alternative to

putting money in a savings bank account.

3. Fixed income or debt mutual funds:

These funds invest a majority of the money in debt -

fixed income i.e. fixed coupon bearing instruments like government securities,

bonds, debentures, etc. They have a low-risk-low-return outlook and are ideal

for investors with a low risk appetite looking at generating a steady income.

However, they are subject to credit risk.

4. Balanced funds:

As the name suggests, these are mutual fund schemes

that divide their investments between equity and debt. The allocation may keep

changing based on market risks. They are more suitable for investors who are

looking at a combination of moderate returns with comparatively low risk.

5. Hybrid / Monthly Income Plans

(MIP):

These funds are similar to balanced funds but the

proportion of equity assets is lesser compared to balanced funds. Hence, they

are also called marginal equity funds. They are especially suitable for

investors who are retired and want a regular income with comparatively low

risk.

6. Gilt funds:

These funds invest only in government securities. They

are preferred by investors who are risk averse and want no credit risk

associated with their investment. However, they are subject to high interest

rate risk.

5. Write a short note on venture capital?

‘Venture Capital’ is an important source of finance for those

small and medium- sized firms, which have very few avenues for raising funds. Although

such a business firm may possess a huge potential for earning large profits in

the future and establish itself into a larger enterprise. But the common

investors are generally unwilling to invest their funds in them due to risk

involved in these types of investments. In order to provide financial support

to such entrepreneurial talent and business skills, the concept of venture

capital emerged. In a way, venture capital is a commitment of capital, or

shareholdings, for the formation and setting-up of small scale enterprises at

the early stages of their lifecycle.

Features of

Venture Capital

1) For New

Entrant: Venture Capital investment is generally made in new

enterprises that use new technology to produce new products, in expectation of

high gains or sometimes, spectacular returns.

2) Continuous Involvement: Venture capitalists continuously involve themselves with the client’s investments, either by providing loans or managerial skills or any other support.

3) Mode of Investment: Venture capital is basically an equity financing method, the investment being made in relatively new companies when it is too early to go to the capital market to raise funds. In addition, financing also takes the form of loan finance/ convertible debt to ensure a running yield on the portfolio of the venture capitalists.

4) Long-term Capital: The basic objective of a venture capitalist is to make a capital gain on equity investment at the time of exit, and regular return on debt financing. It is a long-term investment in growth- oriented small/medium firms. It is a long-term capital that is an injected to enable the business to grow at a rapid pace, mostly from the start-up stage.

5) Hands-On Approach: Venture capital institution take active part in providing value – added services such as providing business skills, etc., to investee firms. Thy do not interfere in the management of the firms nor do they acquire a majority / controlling interest in the investee firms. The rationale for the extension of hands- on management is that venture capital investments tend to be highly non- liquid.

6) High risk- return Ventures: Venture capitalists finance high risk-return ventures. Some of the ventures yield very high return in order to compensate for the heavy risks related to the ventures. Venture capitalists usually make hug capital gains at the time of exit.

7) Source of Finance: Venture capitalists usually finance small and medium- sized firms during the early stages of their development, until they are established and are able to raise finance from the conventional industrial finance market. Many of these firms are new, high technology- oriented companies.

8) Liquidity: Liquidity of venture capital investment depends on the success or otherwise of the new venture or product. Accordingly, there will be higher liquidity where the new ventures are highly successful.

2) Continuous Involvement: Venture capitalists continuously involve themselves with the client’s investments, either by providing loans or managerial skills or any other support.

3) Mode of Investment: Venture capital is basically an equity financing method, the investment being made in relatively new companies when it is too early to go to the capital market to raise funds. In addition, financing also takes the form of loan finance/ convertible debt to ensure a running yield on the portfolio of the venture capitalists.

4) Long-term Capital: The basic objective of a venture capitalist is to make a capital gain on equity investment at the time of exit, and regular return on debt financing. It is a long-term investment in growth- oriented small/medium firms. It is a long-term capital that is an injected to enable the business to grow at a rapid pace, mostly from the start-up stage.

5) Hands-On Approach: Venture capital institution take active part in providing value – added services such as providing business skills, etc., to investee firms. Thy do not interfere in the management of the firms nor do they acquire a majority / controlling interest in the investee firms. The rationale for the extension of hands- on management is that venture capital investments tend to be highly non- liquid.

6) High risk- return Ventures: Venture capitalists finance high risk-return ventures. Some of the ventures yield very high return in order to compensate for the heavy risks related to the ventures. Venture capitalists usually make hug capital gains at the time of exit.

7) Source of Finance: Venture capitalists usually finance small and medium- sized firms during the early stages of their development, until they are established and are able to raise finance from the conventional industrial finance market. Many of these firms are new, high technology- oriented companies.

8) Liquidity: Liquidity of venture capital investment depends on the success or otherwise of the new venture or product. Accordingly, there will be higher liquidity where the new ventures are highly successful.

Process:

Deal Origination:

Venture capital financing begins with origination of a deal. For venture

capital business, stream of deals is necessary. There may be various sources of

origination of deals. One such source is referral system in which deals are

referred to venture capitalists by their parent organizations, trade partners,

industry association, friends, etc.

Screening:

Venture capitalist in his endeavour to choose the best ventures first of

all undertakes preliminary scrutiny of all projects on the basis of certain

broad criteria, such as technology or product, market scope, size of

investment, geographical location and stage of financing.

Evaluation:

After a proposal has passed the preliminary screening, a detailed

evaluation of the proposal takes place. A detailed study of project profile,

track record of the entrepreneur, market potential, technological feasibility

future turnover, profitability, etc. is undertaken.

Deal Negotiation:

Once the venture is found viable, the venture capitalist negotiates the

terms of the deal with the entrepreneur. This it does so as to protect its

interest. Terms of the deal include amount, form and price of the investment.

Post Investment Activity:

Once the deal is financed and the venture begins working, the venture

capitalist associates himself with the enterprise as a partner and collaborator

in order to ensure that the enterprise is operating as per the plan.

Exit Plan:

The last stage of venture capital financing is the exit to realise the

investment so as to make a profit/minimize losses. The venture capitalist

should make exit plan, determining precise timing of exit that would depend on

an a myriad of factors, such as nature of the venture, the extent and type of

financial stake, the state of actual and potential competition, market

conditions, etc.

6. Explain the general obligation and regulation of

merchant banking?

Obligation

# 1. Merchant Banker not to Associate with any Business other than that of the

Securities Market:

No

merchant banker, other than a bank or a public financial institution, who has

been granted a certificate of registration under these regulations, shall

[after June 30th, 1998] carry on any business other than that in the securities

market.

Obligation

# 2. Maintenance of Book of Accounts, Records, etc.:

Every merchant banker shall keep and maintain

the following books of accounts, records and documents, namely:

(a) A

copy of balance sheet as at the end of each accounting period;

(b) A

copy of profit and loss account for that period:

(c) A copy of the auditor’s report on the

accounts for that period; and

(d) a

statement of financial position.

Every

merchant banker shall intimate to the Board the place where the books of

accounts, records and documents are maintained. Without prejudice to

sub-regulation (I), every merchant banker shall, after the end of each

accounting period furnish to the Board copies of the balance sheet, profit and

loss account and such other documents for any other preceding five accounting

years when required by the Board.

Obligation

# 3. Submission of Half-yearly Results:

Every

merchant banker shall furnish to the Board half-yearly unaudited financial

results when required by the Board with a view to monitor the capital adequacy

of the merchant banker.

Obligation

# 4. Maintenance of Books of Accounts, Records and other

Documents:

The

merchant banker shall preserve the books of accounts and other records and

documents for a minimum period of five years.

Obligation

# 5. Report on Steps taken on Auditor’s Report:

Every

merchant banker shall within two months from the date of the auditors’ report

take steps to rectify the deficiencies, made out in the auditor’s report.

Obligation

# 6. Appointment

of Lead Merchant Bankers:

All issues should be managed by at

least one merchant banker functioning as the lead merchant banker:

Provided

that, in an issue of offer of rights to the existing members with or without

the right of renunciation the amount of the issue of the body corporate does

not exceed rupees fifty lakhs, the appointment of a lead merchant banker shall

not be essential. Every lead merchant banker shall before taking up the

assignment relating to an issue, enter into an agreement with such body

corporate setting out their mutual rights, liabilities and obligations relating

to such issue and in particular to disclosures, allotment and refund.

Obligation

# 7. Restriction

on Appointment of Lead Managers:

The

number of lead merchant bankers may not, exceed in case of any issue of;

{kind=link}

Obligation

# 8. Responsibilities of Lead Managers:

(1) No

lead manager shall agree to manage or be associated with any issue unless his

responsibilities relating to the issue mainly, those of disclosures, allotment

and refund are clearly, defined, allocated and determined and a statement

specifying such responsibilities is furnished to the Board atleast one month

before the opening of the issue for subscription:

Provided

that, where there are more than one lead merchant banker to the issue the

responsibilities of each of such lead merchant banker shall clearly be

demarcated and a statement specifying such responsibilities shall be furnished

to the Board atleast one month before the Opening of the issue for Subscription.

No lead merchant banker shall, agree to manage the issue made by anybody

corporate, if such body corporate is an associate of the lead merchant banker.

Obligation

# 9. Lead Merchant Banker not to Associate with a Merchant

Banker without Registration:

A lead

merchant banker shall not be associated with any issue if a merchant banker who

is not holding a certificate is associated with the issue.

Obligation

# 10. Underwriting Obligations:

In

respect of every issue to be managed, the lead merchant banker holding a

certificate under Category I shall accept a minimum underwriting obligation of

five per cent of the total underwriting commitment or rupees twenty-five lacs,

whichever is less:

Provided

that, if the lead merchant banker is unable to accept the minimum underwriting

obligation, that lead merchant banker shall make arrangement for having the

issue underwritten to that extent by a merchant banker associated with the

issue and shall keep the Board informed of such arrangement.

Obligation

# 11. Submission

of Due Diligence Certificate:

The

lead merchant banker, who is responsible for verification of the contents of a

prospectus or the letter of offer in respect of an issue and the reasonableness

of the views expressed therein, shall submit to the Board atleast two weeks

prior to the opening of the issue for subscription, a due diligence certificate

in Form C.

Obligation

# 12. Documents

to be Furnished to the Board:

(1) The lead manager responsible for the issue

shall furnish to the Board, the following documents, namely:

(i) Particulars of the issue;

(ii)

Draft prospectus or where there is an offer to the existing shareholders, the

draft letter of offer;

(iii)

Any other literature intended to be circulated to the investors, including the

shareholders; and

(iv) Such

other documents relating to prospectus or letter of offer, as the case may be.

The

documents referred to in sub-regulation (1) shall be furnished atleast two

weeks prior to date of filing of the draft prospectus or the letter of offer,

as the case may be, with the Registrar of Companies or with the Regional Stock

Exchanges, or with both.The lead manager shall ensure that the modifications

and suggestions, if any, made by the Board on the draft prospectus or the

letter of offer, as the case may be, with respect to information to be given to

the investors are incorporated therein.

Obligation

# 13. Continuance of Association of Lead Manager with an Issue:

The

lead manager undertaking the responsibility for refunds or allotment of

securities in respect of any issue shall continue to be associated with the

issue till the subscribers have received the share or debenture certificates of

refund or excess application money. Provided that where a person other than the

lead manager is entrusted with the refund or allotment of securities in respect

of any issue, the lead manager shall continue to be responsible for ensuring

that such other person discharges the requisite responsibilities in accordance

with the provisions of the Companies Act and the listing agreement entered into

by the body corporate with the stock exchange.

Obligation

# 14. Acquisition

of Shares Prohibited:

No

merchant banker or any of its directors, partner or manager or principal

officer shall either on their respective accounts or through their associates

or relatives enter into any transaction in securities of bodies corporate on

the basis of unpublished price sensitive information obtained by them during

the course of any professional assignment either from the clients or otherwise.

Obligation

# 15. Information to the Board:

Every

merchant banker shall submit to the Board complete particulars of any

transaction for acquisition of securities of anybody corporate whose issue is

being managed by that merchant banker within fifteen days from the date of

entering into such transaction.

Obligation

# 16. Disclosures to the Board:

A merchant banker shall disclose to the Board

as and when required, the following information, namely:

(i)

His responsibilities with regard to the management of the issue;

(ii) Any

change in the information or particulars previously furnished, which have a

bearing on the certificate granted to it;

(iii)

The names of the body corporate whose issues he has managed or has been

associated with;

(iv)

The particulars relating to breach of the capital adequacy requirement;

(v)

Relating to his activities as a manager, underwriter, consultant or adviser to

an issue as the case may be.

Obligation

# 17. Appointment

of Compliance Officer:

Every

merchant banker shall appoint a compliance officer who shall be responsible for

monitoring the compliance of the Act, rules and regulations, notifications,

guidelines, instructions, etc. issued by the Board or the Central Government

and for redressal of investors’ grievances. The compliance officer shall

immediately and independently report to the Board any non-compliance observed

by him and ensure that the observations made or deficiencies pointed out by the

Board on/in the draft prospectus or the Letter of Offer as the case may be, do

not recur.

Obligation

# 18. Board’s

right to Inspect:

The Board may appoint one or more persons as

inspecting authority to undertake inspection of the books of accounts, records

and documents of the merchant banker for any of the following purposes:

(a) To

ensure that the books of account are being maintained in the manner required.

(b)

That the provisions of the Act, rules, regulations are being complied with;

(c) To

investigate into the complaints received from investors, other merchant bankers

or any other person on any matter having a bearing on the activities of the

merchant banker, and

(d) To

investigate suo moto in the interest of securities business or investors

interest into the affairs of the merchant banker.

Obligation

# 19. Obligations

of Merchant Banker on Inspection by the Board:

It

shall be the duty of every director, proprietor, partner, officer and employee

of the merchant banker, who is being inspected, to produce to the inspecting

authority such books, accounts and other documents in his custody or control and

furnish him with the statements and information relating to his activities as a

merchant banker within such time as the inspecting authority may require.

7. How does the SBI differ from other nationalized

banks in India?

Ownership

SBI is almost wholly owned by the

RBI, while the subsidiary banks are almost owned by the SBI. On the other hand

nationalised banks are almost wholly owned by the Government of India.

Functioning

The SBI besides carrying out its

normal banking functions also acts as an agent of the RBI According to the

Section 45 of the RBI Act, 1934, “The Reserve Bank shall appoint the State Bank

as its sole agent at all places in India where it does not have any office or

branch of its banking department and there is a branch of the State Bank or

branch of a subsidiary bank. This privilege has not been conferred upon the

nationalised banks. However, after the enforcement of the Banks Laws

(Amendment) Act, 1983, the RBI can appoint any nationalised bank to act as an

agent at all places where it has a branch for the following purposes:

1. Paying, receiving, collecting

and remitting money, bullion and securities on behalf of the Government in

India and,

2. Undertaking and transacting any other business entrusted by the Reserve Bank from time to time.

Organizational Structure The organisational structure of the State Bank of India is somewhat different from the other nationalised banks. It has a well-defined system of decentralisation of authority. The whole country has been divided into nine circles for administrative control purposes The Head Offices of each circle is known as Local Head Office with a Local Board of Directors which has a statutory status. Each circle has been further divided into a number of Regions. There is a Chief General Manager (formerly known as the Secretary and Treasurer) for each Circle He is the Chief Executive for his circle and has under him Regional Managers for the different regions in his circle. The Chief General Manager enjoys vast powers for control over branches and has also extensive discretionary powers regarding loans and advances. All this has resulted in taking the operational control nearer to the area of operation. The Bank is further trying to strengthen the Regional Offices so as to reduce the span of control of the controlling authority (i.e., the Chief General Manager), leading to further decentralisation.

2. Undertaking and transacting any other business entrusted by the Reserve Bank from time to time.

Organizational Structure The organisational structure of the State Bank of India is somewhat different from the other nationalised banks. It has a well-defined system of decentralisation of authority. The whole country has been divided into nine circles for administrative control purposes The Head Offices of each circle is known as Local Head Office with a Local Board of Directors which has a statutory status. Each circle has been further divided into a number of Regions. There is a Chief General Manager (formerly known as the Secretary and Treasurer) for each Circle He is the Chief Executive for his circle and has under him Regional Managers for the different regions in his circle. The Chief General Manager enjoys vast powers for control over branches and has also extensive discretionary powers regarding loans and advances. All this has resulted in taking the operational control nearer to the area of operation. The Bank is further trying to strengthen the Regional Offices so as to reduce the span of control of the controlling authority (i.e., the Chief General Manager), leading to further decentralisation.

Salary

and Perks

There are 4 additional increments

in SBI at the time of joining itself as compared to any other bank. Hence, you

get around INR 3700 per month (Basic+DA) more salary in SBI. Perks given to

officers in SBI are much more than any other bank.

Lease House Facility

Lease house facilities are much

better in SBI as it has much higher rent ceilings as compared to other banks.

Exposure

SBI PO gets much wider range of

exposure as compared to PO of any other bank, ranging from specialized outfits

on credit, forex to treasury etc.

Opportunities for Foreign Postings

There is always a possibility of

foreign posting as PO in SBI, with the increasing global presence of SBI and

its focus on global presence.

8. Discuss the functions of NABARD? (Guide- 18, 19)

Credit Functions:

- Framing policy and

guidelines for rural financial institutions.

- Providing credit facilities

to issuing organizations

- Monitoring the flow of

ground level rural credit.

- Preparation of credit plans

annually for all districts for identification of credit potential.

Development Functions:

- Help cooperative banks and

Regional Rural Banks to prepare development actions plans for themselves.

- Help Regional Rural Banks

and the sponsor banks to enter into MoUs with state governments and

cooperative banks to improve the affairs of the Regional Rural Banks.

- Monitor implementation of

development action plans of banks.

- Provide financial support

for the training institutes of cooperative banks, commercial banks and

Regional Rural Banks.

- Provide financial assistance

to cooperative banks for building improved management information system,

computerisation of operations and development of human resources.

Supervisory Functions:

- Undertakes inspection of

Regional Rural Banks (RRBs) and Cooperative Banks (other than

urban/primary cooperative banks) under the provisions of Banking

Regulation Act, 1949.

- Undertakes inspection of

State Cooperative Agriculture and Rural Development Banks (SCARDBs) and

apex non- credit cooperative societies on a voluntary basis.

- Provides recommendations to

Reserve Bank of India on issue of licenses to Cooperative Banks, opening

of new branches by State Cooperative Banks and Regional Rural Banks

(RRBs).

- Undertakes portfolio

inspections besides off-site surveillance of Cooperative Banks and

Regional Rural Banks (RRBs).

9. Outline the Guidelines issued by RBI prescribing the prudential norms

of NBFC?

The Bank has issued detailed directions on prudential

norms, vide Non-Banking Financial (Deposit Accepting or Holding) Companies

Prudential Norms (Reserve Bank) Directions, 2007, Non-Systemically Important

Non-Banking Financial (Non-Deposit Accepting or Holding) Companies Prudential

Norms (Reserve Bank) Directions, 2015 and Systemically Important Non-Banking

Financial (Non-Deposit Accepting or Holding) Companies Prudential Norms

(Reserve Bank) Directions, 2015. Applicable regulations vary based on the

deposit acceptance or systemic importance of the NBFC. The directions inter

alia, prescribe guidelines on income recognition, asset classification and

provisioning requirements applicable to NBFCs, exposure norms, disclosures in

the balance sheet, requirement of capital adequacy, restrictions on investments

in land and building and unquoted shares, loan to value (LTV) ratio for NBFCs

predominantly engaged in business of lending against gold jewellery, besides

others. Deposit accepting NBFCs have also to comply with the statutory

liquidity requirements.

10. What are the features of SEBI guidelines regarding Mutual Funds?

a. Categorization of schemes

into five groups – Equity, Debt, Hybrid, Solution Oriented, Others

b. To ensure uniformity,

large, mid and small cap has been defined clearly

c. There is a lock-in period

specified for solution-oriented schemes

d. Permission of only one scheme in each category,

except for Index Funds/ Exchange Traded Funds (ETF), Sectoral/Thematic Funds

and Funds of Funds.

11. What are

the recent changes regarding the registration of Merchant Bankers?

For registration

as a Merchant Banker, an applicant is required to pay a non-refundable

application fee of Rs.50,000/- by way of demand draft drawn in favour of

‘Securities and Exchange Board of India’, payable at Mumbai. The application in

Form A along with Additional Information Sheet (available under ‘Application

for registration / renewal of intermediaries > Merchant Banker- How to

apply’ on SEBI Website: www.sebi.gov.in) need to be submitted to the below

mentioned address: Market Intermediaries Regulations and Supervision Department

Division 5 Securities and Exchange Board of India, SEBI Bhavan, Plot No. C4-A,

‘G’ Block, Bandra-Kurla Complex, Bandra (E), Mumbai - 400 051.

12. What are the obligations of Listed Companies?

1. Material disclosures

The 2015 Regulations have rearranged and augmented the

existing disclosure obligations of a listed entity. Regulation 30 which

corresponds to Clause 36 of the equity listing agreement requires every listed

entity to make such event based and information disclosures which are

"material" in the opinion of the board of directors.

2. Stricter governance requirements on board of

directors

The 2015 Regulations in certain instances moves beyond

mere alignment with governance requirements and thresholds as provided under

the Companies Act and adopts a stricter approach towards the composition of

board, its committees and the duties of directors. It tends to retain the

higher requirements of Clause 49 of the equity listing agreement as well as amends

some of the voluntary guidelines, to make them mandatory.

3. Related Party Transactions

Related party transactions ("RPTs")

continue to garner constant attention for Indian companies. The Companies Act

initially mandated special resolution for specific RPTs exceeding prescribed

threshold. The Ministry of Corporate Affairs through an amendment in 2015

replaced the requirement of special resolution by an ordinary resolution. It

also issued a circular7 clarifying that only such related

parties who are related to the particular transaction should abstain from

voting on the proposed resolution.

4. Corporate governance for listed start-ups

In August 2015, SEBI amended the SEBI (Issue of

Capital and Disclosure Requirements) Regulations, 2009 to enable listing of

certain categories of start-ups8 without undergoing an initial

public offer. The underlying objective was to liberalize the stricter listing

compliances and disincentives start-ups opting to list on foreign stock

exchanges. These start-ups must alter their structure into public companies

prior to listing. Further, they can raise capital only through rights issue and

private placement (which were otherwise available under Companies Act) and

cannot invite retail investments or make any public offer.

13. The SEBI is trying to integrate functioning of stock exchanges for

better investor service. Discuss.

- the

exchange provides a fair, equitable and growing market to investors

- the

exchange’s organisation, systems and practices are in accordance with the

Securities Contracts (Regulation) Act (SC(R) Act), 1956 and rules framed

thereunder

- the

exchange has implemented the directions, guidelines and instructions

issued by the SEBI from time to time

- The

exchange has complied with the conditions, if any, imposed on it at the

time of renewal/ grant of its recognition under section 4 of the SC(R)

Act, 1956.

Based on

the observations/suggestions made in the inspection reports, the exchanges are

advised to send a compliance report to SEBI within one month of the receipt of

the inspection report by the exchange and thereafter quarterly reports

indicating the progress made by them in implementing the suggestions contained

in the inspection report. The SEBI nominee directors and public representatives

on the governing board/council of management of the stock exchanges also pursue

the matters in the meetings of the governing board/council of management. If

the performance of the exchanges whose renewal of recognition is due, is not

found satisfactory, the SEBI grants further recognition for a short period

only, subject to fulfilment of certain conditions.

14. Write a note on evolution of Commercial Banking?

The

commercial banking industry in India started in 1786 with the establishment of

the Bank of Bengal in Calcutta. British India at the time established three

Presidency banks, namely,

1. Bank of

Bengal (established in 1809)

2. Bank of

Bombay (established in 1840)

3. Bank of

Madras (established in 1843)

In 1921,

the three Presidency banks were amalgamated to form the Imperial Bank of India,

which took up the role of a commercial bank, a bankers’ bank and a banker to

the Government. The Imperial Bank of India was established mainly with European

shareholders. After the establishment of the Reserve Bank of India (RBI) as the

central bank of the country in 1935, the role of the Imperial Bank of India

came to an end. Commercial banks in India have traditionally focused on meeting

the short-term financial needs of industry, trade and agriculture. However, the

increasing diversification of the Indian economy, the range of services

extended by commercial banks. Currently, commercial banks in India are

categorised into five different groups according to their ownership and/or

nature of operation:

1.

State

Bank of India and its Associates

2.

Nationalised

Banks

3.

Private

Sector Banks

4.

Foreign

Banks

5.

Regional

Rural Banks

15. What are the conditions for

recognition of a stock exchange?

(i)

|

the qualifications for membership of stock

exchanges;

|

|

(ii)

|

the manner in which contracts shall be entered

into and enforced as between members;

|

|

(iii)

|

the representation of the Central Government on

each of the stock exchange by such number of persons not exceeding three as

the Central Government may nominate in this behalf; and

|

|

(iv)

|

the maintenance of accounts of members and their

audit by chartered accountants whenever such audit is required by the Central

Government.

|

(3) Every grant of recognition to a stock exchange

under this section shall be published in the Gazette of India and also in the

Official Gazette of the State in which the principal office as of the stock

exchange is situate, and such recognition shall have effect as from the date of

its publication in the Gazette of India.

(4) No application for the grant of recognition

shall be refused except after giving an opportunity to the stock exchange

concerned to be heard in the matter; and the reasons for such refusal shall be

communicated to the stock exchange in writing.

(5) No rules of a recognised stock exchange

relating to any of the matters specified in sub-section (2) of section 3 shall

be amended except with the approval of the Central Government.

16. Explain

the different ways of making fresh issues of securities?

Public Issue

This is the most common way to issue securities to the

general public. Through an IPO, the company is able to raise funds. The

securities are listed on a stock exchange for trading purposes.

Rights Issue

When a company wants to raise more capital from

existing shareholders, it may offer the shareholders more shares at a price

discounted from the prevailing market price. The number of shares offered is on

a pro-rata basis. This process is known as a Rights Issue.

Preferential

Allotment

When a listed company issues shares to a few

individuals at a price that may or may not be related to the market price, it

is termed a preferential allotment. The company decides the basis of allotment

and it is not dependent on any mechanism such as pro-rata or anything else.

Secondary

Market

The secondary market is where existing shares,

debentures, bonds, etc. are traded among investors. Securities that are offered

first in the primary market are thereafter traded on the secondary market. The

trade is carried out between a buyer and a seller, with the stock exchange

facilitating the transaction. In this process, the issuing company is not

involved in the sale of their securities.

Composite Issue:

A composite issue is one in which an already listed company offers shares on

the public-cum-rights basis and makes concurrent allotment of the shares.

Bonus Issue:

As the name itself suggests, it is the free additional shares distributed to

the current shareholders in the proportion of the fully paid-up equity shares

held by them on a particular date. The issue of these shares is made out of the

company’s free reserves or securities premium account.

17. Difference

between equity shares and preference shares?

Points of

difference

|

Equity Shares

|

Preference Shares

|

1. Term of financing

|

Used as a method of long term

financing

|

Used for both long term and medium

term financing.

|

2. Nature of return

|

Rate of return is fluctuating,

depending upon the earning

|

Dividend at fixed rate may be paid

or accumulated.

|

3. Owners

|

Equity shareholders are the owners.

They have voting rights.

|

These shareholders are not owners.

They have no voting rights.

|

4. Reedeemability

|

They are not subject to redemption

during the lifetime of the company.

|

It can be redeemed after achieving

the purpose or at the end of a certain period.

|

5. Type of Investors

|

Suitable for those investors who

are adventurous by nature.

|

It has appeal for relatively less

adventurous investors.

|

6. Right of receiving dividend

|

Residual claimant. Rank next to

preference shares.

|

Entitled for first preference

|

7. Right of receiving back invested

capital during liquidation.

|

Entitled for first preference

|

Entitled for first preference

|

8. Financial burden

|

Payment of equity dividends is

optional. It is dependent on the discretion of the Board of Directors.

Therefore there is no fixed financial commitment.

|

Payment of preference dividend is a

fixed financial commitment.

|

9. Voting rights

|

Enjoy voting rights

|

Do not enjoy voting rights

|

10. Reduction of capital

|

By reorganization

|

By repayment

|

11. Denomination

|

Generally of lower denomination.

|

Generally of higher denomination.

|

12. Type of investors.

|

Even small investors can invest

because of the lower denomination.

|

Preferred by medium and large

investors. Small investors would find it difficult to invest because of the

higher denomination.

|

13. Borrowing capacity

|

Strengthens borrowing capacity.

|

Reduces borrowing capacity.

|

14. Capitalization

|

There are chances for

over-capitalisation.

|

Lesser chances for

over-capitalization.

|

18. Comment on modern customer

relationship and bankers?

The Major Benefits of Analytical

CRM to Banks are

1. Customer Retention 2. Fraud Detection 3.

Optimizing marketing efforts as per customer life time value 4. Credit Risk

Analysis 5. Segmentation and targeting 6. Development of customized new

products matching the specific preferences and priorities of customers.

CRM to banks are

1.

Providing efficient customer communication across a variety of channels

2. Online

services to reduce customer service costs

3. Providing

access to customer data while interacting with customers.

Thus, CRM

can be understood as a catalyst enabling transformation of Banking from

Traditional Transactional banking to Relationship Banking by use of technology.

19. Define Assets and Liabilities Management?

Meaning

of Asset Liability Management (ALM):

Asset Liability

Management in practical terms amounts to management of total balance sheet

items, its size and quality. It involves conscious decisions with regard to

asset liability structure in order to maximize interest earnings within the

frame work of perceived risk with quantification of risk.

ALM encompasses the

process of managing Net interest Margin (NIM), within the overall risk. It

calls for an integrated approach to decision making with regard to type

(demand/time maturities) and size (portfolios) of financial assets and

liabilities and their mix and volumes (turnover). The success of ALM hinges on

matching of assets and liabilities in terms of Rate and maturity to optimize

the yield and maintain/improve the NIM.

A sound ALM system for the bank

should include:

1. Interest rate

movement and outlook,

2. Pricing of assets

and liabilities,

3. Review of investment

portfolio and credit risk management,

4. Review of investment

of foreign exchange operations,

5. Management of

liquidity Risk,

6. Management of NIM

and of balance sheet ratios, and

7. Formulation of budgets

and operational planning.

20. What are specialised financial institutions and

give examples?

- Specialised

Financial Institutions (SFIs):- are

the institutions which have been set up to serve the increasing financial

needs of commerce and trade in the area of venture capital, credit rating

and leasing, etc.

- IFCI Venture Capital Funds Ltd (IVCF):- formerly known as Risk

Capital & Technology Finance Corporation Ltd (RCTC), is a subsidiary

of IFCI Ltd. It was promoted with the objective of broadening

entrepreneurial base in the country by facilitating funding to ventures

involving innovative product/process/technology. Initially, it started

providing financial assistance by way of soft loans to promoters under

its 'Risk Capital Scheme' . Since 1988, it also started providing

finance under 'Technology Finance and Development Scheme' to projects for

commercialisation of indigenous technology for new processes, products,

market or services. Over the years, it has acquired great deal of

experience in investing in technology-oriented projects.

- ICICI Venture Funds Ltd:- formerly known as Technology Development

& Information Company of India Limited (TDICI), was founded in 1988

as a joint venture with the Unit Trust of India. Subsequently, it became

a fully owned subsidiary of ICICI. It is a technology venture finance

company, set up to sanction project finance for new technology ventures.

The industrial units assisted by it are in the fields of computer,

chemicals/polymers, drugs, diagnostics and vaccines, biotechnology,

environmental engineering, etc.

- Tourism Finance Corporation

of India Ltd. (TFCI):- is a specialised financial institution set up by

the Government of India for promotion and growth of tourist industry in

the country. Apart from conventional tourism projects, it provides

financial assistance for non-conventional tourism projects like amusement

parks, ropeways, car rental services, ferries for inland water transport,

etc.

21.

What is rural financing and why it is important?

Rural Finance is

one of the biggest agricultural, commercial and

industrial finance brokerage company’s operating

throughout England, Scotland, Wales and Northern Ireland. Getting finance is

the corner stone of every business and because every business is

different Rural Finance offers bespoke

services tailored to each company’s needs.

Rural financing is

provided through cooperatives and self-help groups. This strategy is highly

beneficial to individuals associated with non-market enterprises or household

businesses. Whether such institutions are governmental or NGOs, the self-help

group can make them profitable by availing resources. People from rural areas

in India have shown significant interest in modern methods of farming. They also

seek other areas of investment such as the stock market or chit funds.

Self-help groups and micro financing in combination with rural banking,

cooperatives, entrepreneur agencies, and small-scale investments present a safe

place for people to invest. Microfinance is not limited to loans and deposits

because it has wide socioeconomic impacts on health, education, and poverty

alleviation. Self-help group consists of groups of individuals that take up

different economic activities in combination. The activities taken up by these

groups include poultry farming, food processing, and vegetable selling among

others in the agricultural supply chain.

22. Describe the role of FDI in India? (Guide- 41)

FDI

plays an important role in the economic development of a country. The capital

inflow of foreign investors allows strengthening infrastructure, increasing

productivity and creating employment opportunities in India. Additionally, FDI

acts as a medium to acquire advanced technology and mobilize foreign exchange

resources. Availability of foreign exchange reserves in the country allows RBI

(the central banking institution of India) to intervene in the foreign exchange

market and control any adverse movement in order to stabilize the foreign

exchange rates. As a result, it provides a more favourable economic environment

for the development of Indian economy.

1) Helps in Balancing International Payments:

FDI is the major source of foreign exchange inflow in

the country. It offers a supreme benefit to country’s external borrowings as

the government needs to repay the international debt with the interest over a

particular period of time. The inflow of foreign currency in the economy allows

the government to generate adequate resources which help to stabilize the BOP

(Balance of Payment).

2) FDI boosts development in various fields:

For the development of an economy, it is important to

have new technology, proper management and new skills. FDI allows bridging of

the technology gap between foreign and domestic firms to boost the scale of

production which is beneficial for the betterment of Indian economy. Thus, FDI

is also considered an asset to the economy.

3) FDI & Employment:

FDI allows foreign enterprises to establish their

business in India. The establishment of these enterprises in the country

generates employment opportunities for the people of India. Thus, the

government facilitates foreign companies to set up their business entities in

the country to empower Indian youth with new and improved skills.

4) FDI encourages export from host country:

Foreign companies carry a broad international

marketing network and marketing information which helps in promoting domestic

products across the globe. Hence, FDI promotes the export-oriented activities

that improve export performance of the country.

Apart from these advantages, FDI helps in creating a

competitive environment in the country which leads to higher efficiency and

superior products and services.

23. Write a note on International Capital Market?

A capital market is a system that allocates financial

resources in the form of debt and equity according to their most efficient

uses. Its main purpose is to provide a mechanism to borrow or invest money

efficiently.

MAIN COMPONENTS OF THE INTERNATIONAL CAPITAL MARKET

A. International Bond

Market

Consists of all bonds

sold by issuing companies, governments, and other organizations outside their

own countries. Buyers include medium- to large-size banks, pension funds,

mutual funds, and governments.

1. Types of

International Bonds

a. Eurobond Issued

outside the country in whose currency it is denominated (e.g., Issued in

Venezuela in U.S. dollars, and sold in Britain, France, and Germany). It

accounts for 75-80% of all international bonds. Absence of regulation reduces

the cost of issuing a bond but increases its risk.

b. Foreign Bond Sold

outside borrower’s country and denominated in currency of country in which it

is sold (e.g., Yen-denominated bond issued by German carmaker BMW in Japan’s

bond market). It accounts for 20-25% of all international bonds. Issuers must

meet certain regulatory requirements and disclose details about company activities,

owners, and upper management.

2. Interest Rates: A

Driving Force

a. Borrowers from newly

industrialized and developing countries borrow money from nations where

interest rates are lower.

b. Investors in

developed countries buy bonds in newly industrialized and developing nations to

obtain a higher return.

c. Many emerging

countries see the need to develop their own national markets. Volatility in

currency market hurts projects that earn funds in those currencies and pay

debts in dollars.

B. International Equity

Market

Consists of all stocks

bought and sold outside the issuer’s home country. Companies and governments

issue equity and buyers include other companies, banks, mutual funds, pension

funds, and individuals.

1. Spread of

Privatization

a. A single

privatization often places billions of dollars of new equity on stock markets.

b. Increased

privatization in Europe is expanding worldwide equity. European Union

integration has made investors willing to invest in stocks from other European

nations.

2. Economic Growth in

Developing Countries

a. Growth in newly

industrialized and developing countries contributes to growth in the

international equity market.

b. Because of a limited

supply of funds in emerging economies, the international equity market is a

major source of funding.

3. Activity of

Investment Banks

a. Investment banks

facilitate the sale of stock worldwide by bringing together sellers and large

potential buyers.

b. Becoming more common

than listing a company’s shares on another country’s stock exchange.

4. Advent of Cyber

markets

a. Stock markets that

have no central geographic location, but consist of online global trading activities

that allow listing of stocks worldwide for electronic 24-hour trading.

C. Eurocurrency Market

(PPT #9)

1. All the world’s

currencies banked outside their countries of origin are called Eurocurrency and

trade on the Eurocurrency market (e.g., U.S. dollars in Tokyo are called

Eurodollars. British pounds in New York are called Euro pounds). Characterized

by large transactions involving only the largest companies, banks, and

governments.

2. Four Sources of

Deposits:

• Governments with

excess funds from prolonged trade surplus.

• Commercial banks with

excess currency.

• International

companies with excess cash.

• Extremely wealthy

individuals.

3. Eurocurrency market

is valued at around $6 trillion, with London accounting for about 20 percent of

all deposits.

4. Appeal of the

Eurocurrency Market

a. Complete absence of regulation lowers costs. Banks charge borrowers

less and pay investors more but still earn profit.

b. Low transaction

costs because transactions are large.

c. Interbank interest

rates are interest rates that the world’s largest banks charge one another for

loans. London Interbank Offer Rate (LIBOR) is the interest rate charged by

London banks to other large banks borrowing Eurocurrency. London Interbank Bid

Rate (LIBID) is the interest rate offered by London banks to large investors

for Eurocurrency deposits.

5. Downside

of Eurocurrency market is greater risk due to a lack of government regulation.

Still, Eurocurrency transactions are fairly safe because of the size of the

banks involved.

24. What is Crossing Cheque? Explain the types of

Crossing?

Crossing of a cheque is nothing but

instructing the banker to pay the specified sum through the banker only, i.e.

the amount on the cheque has to be deposited directly to the bank account of

the payee. Hence, it is not instantly en-cashed by the holder presenting

the cheque at the bank counter.

If any cheque contains such an instruction, it is called a crossed cheque. The crossing of a cheque is done by

making two transverse parallel lines at the top left corner across the face of

the cheque.

Types of Crossing

The way a cheque is crossed specified the

banker on how the funds are to be handled, to protect it from fraud and

forgery. Primarily, it ensures that the funds must be transferred to the bank

account only and not to encash it right away upon the receipt of the cheque.

There are several types of crossing

1.

General

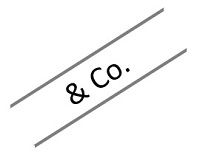

Crossing: When across the face of a cheque two transverse parallel lines

are drawn at the top left corner, along with the words & Co., between the

two lines, with or without using the words not negotiable. When a cheque is

crossed in this way, it is called a general crossing.

{kind=link}

2.

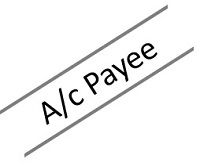

Restrictive

Crossing: When in between the two transverse parallel lines, the words

‘A/c payee’ is written across the face of the cheque, then such a crossing is

called restrictive crossing or account payee crossing. In this case, the cheque

can be credited to the account of the stated person only, making it a non-negotiable

instrument.

{kind=link}

3.

Special

Crossing: A cheque in which the name of the banker is written, across the

face of the cheque in between the two transverse parallel lines, with or

without using the word ‘not negotiable’. This type of crossing is called a

special crossing. In a special crossing, the paying banker will pay the sum

only to the banker whose name is stated in the cheque or to his agent. Hence,

the cheque will be honoured only when the bank mentioned in the crossing orders

the same.

{kind=link}

4.

Not Negotiable

Crossing: When the words not negotiable is mentioned in between the two

transverse parallel lines, indicating that the cheque can be transferred but

the transferee will not be able to have a better title to the cheque.

{kind=link}

5.

Double

Crossing: Double crossing is when a bank to whom the cheque crossed

specially, further submits the same to another bank, for the purpose of

collection as its agent, in this situation the second crossing should indicate

that it is serving as an agent of the prior banker, to whom the cheque was

specially crossed.

The crossing of a cheque is done to ensure

the safety of payment. It is a well-known mechanism used to protect the parties

to the cheque, by making sure that the payment is made to the right payee.

Hence, it reduces fraud and wrong payments, as well as it protects the

instrument from getting stolen or en-cashed by any unscrupulous individual.

25. Explain the functions of central bank?

(i) Bank of issue:

Possesses an exclusive

right to issue notes (currency) in every country of the world. In the initial

years of banking, every bank enjoyed the right of issuing notes. However, this

led to a number of problems, such as notes were over-issued and the currency

system became disorganized. Therefore, the governments of different countries

authorized central banks to issue notes. The issue of notes by one bank has led

to uniformity in note circulation and balance in money supply.

(ii) Government’s banker, agent, and advisor:

Implies that a central

bank performs different functions for the government. As a banker, the central

bank performs banking functions for the government as commercial banks performs

for the public by accepting the government deposits and granting loans to the

government. As an agent, the central bank manages the public debt, undertakes

the payment of interest on this debt, and provides all other services related

to the debt.

(iii) Custodian of cash reserves of commercial

banks:

Implies that the

central bank takes care of the cash reserves of commercial banks. Commercial

banks are required to keep certain amount of public deposits as cash reserve,

with the central bank, and other part is kept with commercial banks themselves.

(iv) Custodian of international currency:

Implies that the

central bank maintains a minimum reserve of international currency. The main

aim of this reserve is to meet emergency requirements of foreign exchange and

overcome adverse requirements of deficit in balance of payments.

(v) Bank of rediscount:

Serve the cash

requirements of individuals and businesses by rediscounting the bills of

exchange through commercial banks. This is an indirect way of lending money to

commercial banks by the central bank. Discounting a bill of exchange implies

acquiring the bill by purchasing it for the sum less than its face value.

(vi) Lender of last resort:

Refer to the most

crucial function of the central bank. The central bank also lends money to

commercial banks. Instead of rediscounting of bills, the central bank provides

loans against treasury bills, government securities, and bills of exchange.

(vii) Bank of central

clearance, settlement, and transfer:

Implies that the

central bank helps in settling mutual indebtness between commercial banks.

Depositors of banks give checks and demand drafts drawn on other banks. In such

a case, it is not possible for banks to approach each other for clearance,

settlement, or transfer of deposits.

(viii) Controller of Credit:

Implies that the

central bank has power to regulate the credit creation by commercial banks. The

credit creation depends upon the amount of deposits, cash reserves, and rate of

interest given by commercial banks. All these are directly or indirectly

controlled by the central bank. For instance, the central bank can influence

the deposits of commercial banks by performing open market operations and

making changes in CRR to control various economic conditions.

26. Explain the services of IBRD?

Technical Assistance - The World Bank Group can provide professional

technical advice that supports legal, policy, management, governance and other

reforms needed for a country's development goals. Our wide-ranging knowledge

and skills are used to help countries build accountable, efficient public

sector institutions to sustain development in ways that will benefit their

citizens over the long term. Bank staff offer advice and support governments in

the preparation of documents, such as draft legislation, institutional

development plans, country-level strategies, and implementation action plans.

We can also assist governments to shape or put new policies and programs in

place.

Reimbursable Advisory Services (RAS) - Through RAS, the Bank can provide clients access to

customized technical assistance on a reimbursable basis, either as a

stand-alone or to complement an existing program. This allows us to provide

advisory services that the client demands, but that the Bank cannot fund in

full within the existing budget envelope. RAS programs have been used in more

than 70 countries since the 1970s. World Bank member countries of all income

levels can access RAS. Clients can be countries and government entities, but

also states and municipalities, state-owned enterprises, civil society

organizations, and multilateral agencies. RAS brochure with project

examples

Economic and Sector Work - In collaboration with country clients and development

partners, Bank country staff gather and evaluate information (data, policies

and statistics) about the existing economy, government institutions or social

services systems. This data provides a starting point for policy and strategic

discussions with borrowers and helps enhance a country's capacity and

knowledge. Studies and analytical reports help us support clients to plan and implement

effective development programs and projects.

Donor Aid Coordination

- The World Bank Group acts on occasion as a coordinator for organized regular interaction among donors (governments, aid agencies, humanitarian groups, foundations, development banks). Activities range from simple information sharing and brainstorming, to co-financing a particular project, to joint strategic programming in a country or region. It also includes the preparation of donor coordination events such as consultative group meetings (joint meetings of partners) focused on a particular issue or country. Other partnership information.

- The World Bank Group acts on occasion as a coordinator for organized regular interaction among donors (governments, aid agencies, humanitarian groups, foundations, development banks). Activities range from simple information sharing and brainstorming, to co-financing a particular project, to joint strategic programming in a country or region. It also includes the preparation of donor coordination events such as consultative group meetings (joint meetings of partners) focused on a particular issue or country. Other partnership information.

27. Explain the objectives of Monetary Policy in

India?

i. To Regulate Money Supply in

the Economy:

Money supply includes

both money in circulation and credit creation by banks. Monetary policy is

farmed to regulate the money supply in the economy by credit expansion or

credit contraction. By credit expansion (giving more loans), the money supply

can be expanded. By credit contraction (giving less loans) money supply can be

decreased.

ii. To Attain Price Stability:

Another major objective

of monetary policy in India is to maintain price stability in the country. It

implies Control over inflation. Price level, is affected by money supply.

Monetary policy regulates money supply to maintain price stability.

iii. To promote Economic

Growth:

An important objective

of monetary policy is to make available necessary supply of money and credit

for the economic growth of the country. Those sectors which are quite

significant for the economic growth are provided with adequate availability of

credit.

iv. To Promote saving and

Investment:

By regulating the rate

of interest and checking inflation, monetary policy promotes saving and

investment. Higher rates of interest promote saving and investment.

v. To Control Business Cycles:

Boom and depression are

the main phases of business cycle. Monetary policy puts a check on boom and

depression. In period of boom, credit is contracted, so as to reduce money

supply and thus check inflation. In period of depression, credit is expanded,

so as to increase money supply and thus promote aggregate demand in the

economy.

vi. To Promote Exports and

Substitute Imports:

By providing

concessional loans to export oriented and import substitution units, monetary

policy encourages such industries and thus help to improve the position of

balance of payments.

vii. To Manage Aggregate

Demand:

Monetary authority tries

to keep the aggregate demand in balance with aggregate supply of goods and

services. If aggregate demand is to be increased than credit is expanded and

the interest rate is lowered down. Because of low interest rate, more people

take loan to buy goods and services and hence aggregate demand increases and

vice-verse.

viii. To Ensure more Credit for

Priority Sector:

Monetary policy aims at

providing more funds to priority sector by lowering interest rates for these

sectors. Priority sector includes agriculture, small- scale industry, weaker

sections of society, etc.

ix. To Promote Employment:

By providing

concessional loans to productive sectors, small and medium entrepreneurs,

special loan schemes for unemployed youth, monetary policy promotes employment.

x. To Develop Infrastructure:

Monetary policy aims at

developing infrastructure. It provides concessional funds for developing infrastructure.

xi. To Regulate and Expand

Banking:

RBI regulates the

banking system of the economy. RBI has expanded banking to all parts of the

country. Through monetary policy, RBI issues directives to different banks for

setting up rural branches for promoting agricultural credit. Besides it,

government has also set up cooperative banks and regional rural banks. All this

has expanded banking in all parts of the country.

28. Explain the Advantages of Foreign Capital?

1. Economic Development Stimulation.

Foreign direct investment can stimulate the target country’s economic development, creating a more conducive environment for you as the investor and benefits for the local industry.

Foreign direct investment can stimulate the target country’s economic development, creating a more conducive environment for you as the investor and benefits for the local industry.

2. Easy International Trade.

Commonly, a country has its own import tariff, and this is one of the reasons why trading with it is quite difficult. Also, there are industries that usually require their presence in the international markets to ensure their sales and goals will be completely met. With FDI, all these will be made easier.

Commonly, a country has its own import tariff, and this is one of the reasons why trading with it is quite difficult. Also, there are industries that usually require their presence in the international markets to ensure their sales and goals will be completely met. With FDI, all these will be made easier.

3. Employment and Economic Boost.

Foreign direct investment creates new jobs, as investors build new companies in the target country, create new opportunities. This leads to an increase in income and more buying power to the people, which in turn leads to an economic boost.